December 2025 Applicable Federal Rates (AFRs): What They Mean for Tax Planning

Key takeaways

- AFRs are the IRS-mandated minimum interest rates for private loans, installment sales, and certain estate planning structures; they update every month.

- Loans made below the applicable AFR risk imputed interest treatment and unintended gift tax consequences under IRC §7872.

- The December 2025 Section 7520 rate is 4.60 percent, which affects present value calculations for GRATs, CRTs, and other trust structures.

- Use the AFR in effect in the month the loan or transfer is signed. The rate does not apply retroactively.

- Document the chosen rate, compounding convention, and IRS Revenue Ruling number in every loan agreement and planning workpaper.

The IRS has released the applicable federal rates December 2025 update. Tax professionals are already reviewing how these numbers affect year-end planning and early 2026 strategies. AFRs influence everything from intra-family loans to installment sales, estate and trust valuations, and corporate financing structures.

Because the rates update every month, staying current is essential for compliance and for capturing planning opportunities.

Applicable Federal Rates (AFRs) are the minimum interest rates the IRS publishes monthly under IRC §1274(d). They are derived from the average market yields of U.S. Treasury obligations and are divided into three term categories: short-term, mid-term, and long-term.

Any private loan, deferred payment arrangement, or trust structure that falls below the applicable rate triggers imputed interest rules, gift tax exposure, or both.

This month's update reflects shifts in financial markets as Treasury yields continue to move. AFRs follow these movements, which means each month can introduce new considerations for clients and businesses.

December 2025 Applicable Federal Rates: AFR Table at a Glance

The following rates are published by the IRS for December 2025 under Revenue Ruling 2025-24. The compounding convention matters: more frequent compounding produces a slightly lower stated minimum rate.

A loan that compounds monthly requires only the monthly-compounding AFR, not the annual rate. Document the compounding method in every loan agreement to match the rate applied.

Source: IRS Revenue Ruling 2025-24. Practitioners should verify the current month's rates at IRS.gov before executing any agreement.

The adjusted AFRs apply to certain deferred payment arrangements and valuation scenarios under specific sections of the tax code. The Section 7520 rate is used for valuing annuities, life estates, remainder interests, and many estate planning structures. Even small changes in these numbers can shift tax outcomes, which is why practitioners treat AFR updates as a monthly planning checkpoint.

Why these rates matter for CPAs and tax attorneys

Structuring loans

AFRs establish the minimum interest rate for loans between related parties. This includes family loans, shareholder loans, and loans between commonly owned businesses. When interest is set below the AFR, the IRS can impute interest under IRC §7872.

Learn how AI tax research tools can help practitioners stay current on these rules.

The consequences run in both directions. The lender is taxed on interest they should have received. The unpaid interest is treated as a gift from lender to borrower, counted against the lender's annual gift exclusion.

For loans above $100,000, this dual exposure is material. Setting the rate at or above the correct AFR tier at closing eliminates both risks.

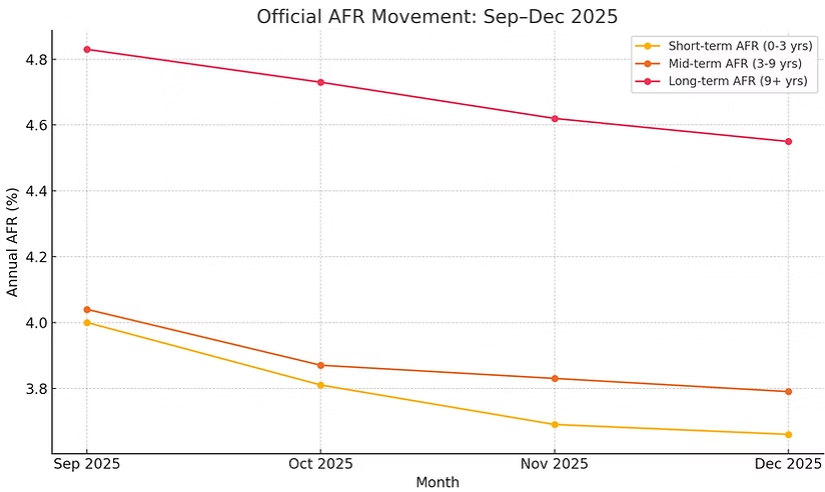

A short-term loan entered into during December can safely use the 3.66 percent annual rate. Setting the rate correctly at signing protects the taxpayer even if market conditions change later.

Example. A parent lends $200,000 to an adult child, structured as a two-year term loan with annual compounding. The applicable short-term AFR for December 2025 is 3.66 percent.

The borrower owes $7,320 in interest for the first year. If the parent charges less than 3.66 percent, the IRS will impute the difference as income to the parent.

The shortfall is also treated as a gift against the parent's annual exclusion.

The same logic applies to shareholder loans and intercompany notes.

The rate and compounding convention in the executed agreement must match the applicable AFR column for the transaction month.

Estate and gift planning effects

AFRs and the Section 7520 rate influence many estate planning techniques. Strategies such as grantor retained annuity trusts, charitable remainder trusts, and intra-family installment sales rely on monthly AFR values. These structures also use Section 7520 rates to calculate present value.

Explore the Bizora knowledge base for primary authority on these structures.

The December Section 7520 rate of 4.60 percent may benefit some strategies and create disadvantages for others. Estate planners often compare multiple months to determine the most favorable timing for a transaction.

For term loans to trusts, the AFR locks in at execution. If trust assets appreciate faster than the note rate, the excess growth passes to beneficiaries outside the taxable estate. Identifying the right month to execute is part of the planning analysis, not an afterthought.

Business and corporate financing considerations

Companies that use intercompany loans, deferred payment contracts, or loans from shareholders must comply with AFR standards. The long-term AFR of 4.55 percent affects interest treatment under several Internal Revenue Code sections, including rules governing original issue discount (OID) under IRC §1274.

For seller-financed sales, the IRS allows use of the lowest AFR within a three-month window ending with the contract or closing month. Solo and small-firm practitioners can review tax research software options for solo CPAs to stay current on these rules efficiently. In a rising rate environment, that look-back can reduce the minimum required rate and lower the OID calculation.

For CFOs and business owners, reviewing debt arrangements during months with meaningful AFR movement can help avoid recharacterization issues and improve tax positioning.

How to apply AFRs in practice

Taxpayers must use the AFR that corresponds to the month the loan or transfer is formalized. AFRs do not apply retroactively. Once a new month begins, a taxpayer generally cannot elect a prior rate unless a specific exception applies.

AFRs also influence valuation work. Present value calculations for annuities, remainder interests, and deferred payments are all based on the AFR or Section 7520 rate. Incorporate a monthly AFR review into your compliance workflow: check the IRS Revenue Ruling before executing any tax-sensitive agreement, not after.

Review how top firms automate tax research and compliance to streamline this process.

Professionals should document the chosen month's rate in their files and ensure all related calculations match. At minimum, every AFR-governed transaction should include:

- A written promissory note or agreement stating the interest rate, compounding convention, and repayment schedule

- The specific IRS Revenue Ruling number confirming the AFR for the transaction month

- Present value or interest calculations referencing the exact AFR and Section 7520 rate used

- Records of actual interest payments made and reported on the lender's return

- For estate planning transactions, a memo connecting the chosen AFR to the valuation methodology

Documentation is not a formality. It is the first line of defense if the IRS questions whether the loan was bona fide or whether a trust valuation was correctly calculated.

Common AFR mistakes and how to avoid them

Practitioners see the same errors repeat across intra-family loans, installment sales, and estate planning transactions. The most costly ones are preventable.

Using the wrong AFR tier: A long-term loan priced at the short-term AFR still exposes the lender to imputed interest. Match the AFR tier to the stated maturity of the instrument, not the expected holding period.

Ignoring compounding: The IRS publishes four compounding variants for each tier. Using the annual rate on a loan that compounds monthly produces a non-compliant stated rate.

The same applies in reverse. Specify the compounding method in the agreement and confirm the corresponding AFR column.

Applying rates retroactively: The AFR for December 2025 applies to agreements executed in December 2025. A January agreement cannot elect December's rate after the fact unless a specific exception applies under the code.

Execute and date agreements in the month whose rate you intend to use.

Failing to document the Revenue Ruling: The IRS publishes AFRs as monthly Revenue Rulings. Workpapers that reference only a percentage without citing the governing ruling are harder to defend on audit.

Include the ruling number in every file.

Assuming AFRs are optional for related-party transactions: For loans between related parties above the de minimis thresholds under IRC §7872, using an AFR-compliant rate is a legal requirement. It is not a planning preference.

Planning considerations for December 2025

Proactive rate management creates compliance protection and strategic advantages. Year-end is a natural planning checkpoint. Many practitioners finalize intra-family loans, trust funding decisions, and intercompany note structures before December 31 to capture the current rate environment.

Compare December's rates against recent prior months before executing. If a lower rate was available in October or November, confirm whether the three-month look-back under IRC §1274 still applies. That window may reduce the required minimum rate.

For transactions that do not qualify, December's rates lock in at execution. Act before month end if current rates are favorable relative to January projections.

Even modest shifts in AFRs have the potential to influence outcomes for high-value transactions. Practitioners handling multiple year-end closings should confirm the rate for each instrument individually rather than applying a single rate across a batch.

December 2025 AFR planning: Key implications and next steps

The applicable federal rates December 2025 release provides a new baseline for loan structuring, estate planning, and corporate finance decisions.

CPAs, tax attorneys, and business owners should review the applicable federal rates December 2025 published figures as part of their year-end strategy. Ensure all agreements and valuations incorporate the correct numbers. Staying current each month reduces IRS exposure and supports stronger, more precise planning.

For professionals who track AFR changes regularly, a research tool that consolidates IRS updates and surfaces governing Revenue Rulings can improve efficiency. Connecting rate changes to planning strategy reduces time spent switching tools.

Bizora AI brings these updates together in one place, grounded in primary authority. Practitioners can move from rate lookup to documented position without switching tools.