Standard vs Itemized Deduction 2026: The Complete Guide for Tax Professionals

The standard vs. itemized decision matters again.

Before the One Big Beautiful Bill Act was passed in July 2025, you probably had a quick answer. The $10,000 SALT cap made itemizing a losing proposition for most filers. But the rules shifted dramatically this year. The SALT cap quadrupled to $40,000, new senior deductions appeared, and the standard deduction amounts increased again.

For the 2025 tax year (returns filed in 2026), every client conversation about deductions requires fresh analysis. The shortcuts that worked last year no longer apply. If you're still running 2024 mental math, you're leaving money on the table for your clients.

This guide breaks down exactly what changed, when each method makes sense, and how to run the numbers efficiently during busy season.

Key Takeaways

- Standard deduction for 2025: $15,750 (single), $31,500 (married filing jointly), $23,625 (head of household)

- SALT cap increased to $40,000 for 2025-2029, up from the previous $10,000 limit, pushing many high-tax-state clients back into itemizing territory

- New senior bonus deduction: Taxpayers 65+ with MAGI below $75,000 (single) or $150,000 (joint) can claim an additional $6,000 to $12,000 through 2028

- Medical expense threshold made permanent at 7.5% of AGI, ending years of uncertainty about potential increases

- Mortgage interest limit of $750,000 is now permanent (previously scheduled to revert to $1 million)

- Charitable contribution changes ahead: A new 0.5% AGI floor begins in 2026, making this year the last for full first-dollar deductions

- Break-even analysis is essential: With the expanded SALT cap, clients who took the standard deduction for years may now benefit from itemizing

Standard vs Itemized Deduction: A Quick Comparison

Before diving into the details, here's how these two methods stack up against each other:

| Factor | Standard Deduction | Itemized Deduction |

|---|---|---|

| What it is | Fixed dollar amount based on filing status | Total of qualifying expenses you claim individually |

| Documentation required | None | Receipts, Form 1098s, donation records, medical bills |

| Complexity | Simple. One number | Requires tracking and calculating multiple categories |

| 2025 amounts | $15,750 to $31,500+ depending on filing status | Varies based on your actual expenses |

| Best for | Renters, low-tax states, seniors with bonus deduction | Homeowners in high-tax states, large charitable givers |

| SALT cap impact | Not applicable | Now up to $40,000 (previously $10,000) |

| Time to claim | Minutes | Hours of documentation |

The fundamental rule: your client claims whichever method produces the larger deduction. They cannot claim both.

What is the Standard Deduction?

The standard deduction is a fixed dollar amount that reduces your client's taxable income. No receipts required, no calculations needed. The IRS sets the amount based on filing status, and your client either qualifies or they don't.

Think of it as a guaranteed deduction every taxpayer can claim simply for filing a return. The IRS essentially says, "We know you had some expenses this year. Instead of making you prove each one, here's a flat amount you can subtract."

For the 2025 tax year, here are the standard deduction amounts:

| Filing Status | 2025 Standard Deduction | 2024 Amount | Year-Over-Year Change |

|---|---|---|---|

| Single | $15,750 | $14,600 | +$1,150 |

| Married Filing Jointly | $31,500 | $29,200 | +$2,300 |

| Married Filing Separately | $15,750 | $14,600 | +$1,150 |

| Head of Household | $23,625 | $21,900 | +$1,725 |

Additional Standard Deduction for Age and Blindness

Taxpayers who are 65 or older or blind qualify for additional amounts on top of the base standard deduction:

| Situation | Additional Amount (2025) |

|---|---|

| Single or Head of Household, age 65+ | $2,000 |

| Single or Head of Household, blind | $2,000 |

| Married (either spouse age 65+) | $1,600 per qualifying spouse |

| Married (either spouse blind) | $1,600 per qualifying spouse |

A married couple where both spouses are 65 or older would add $3,200 to their base amount, bringing their total standard deduction to $34,700.

The New Senior Bonus Deduction (2025-2028)

Here's a provision many tax professionals missed in the OBBBA: a new bonus deduction for seniors that stacks on top of the existing additional amounts.

Taxpayers 65 or older can claim an extra $6,000 ($12,000 for married couples where both qualify) if their modified adjusted gross income falls below $75,000 for single filers, $150,000 for married filing jointly, or $112,500 for head of household. The deduction phases out at 6% of MAGI exceeding these thresholds, disappearing entirely at $175,000 (single) or $250,000 (joint).

This provision runs from 2025 through 2028. For qualifying clients, the numbers become substantial. Unlike the existing 65+ additional standard deduction, this new benefit is available to both itemizers and standard deduction filers.

Example: A married couple, both 66 years old, with MAGI of $140,000:

- Base standard deduction: $31,500

- Additional for age (both spouses): $3,200

- Senior bonus deduction: $12,000

- Total standard deduction: $46,700

That's a powerful number to beat with itemized deductions.

Pros and Cons of the Standard Deduction

Advantages:

- Simplicity. No tracking expenses throughout the year, no digging through receipts at tax time. You find the correct amount for your filing status and subtract it from your income.

- Guaranteed benefit. Your client qualifies even if they have no deductible expenses or no documentation of their spending.

- No audit risk on deduction amounts. The IRS won't question whether your client's standard deduction is accurate because it's a fixed amount.

- Faster tax preparation. Claiming the standard deduction takes minutes, compared with the hours required to itemize.

Disadvantages:

- May leave money on the table. Clients with substantial mortgage interest, property taxes, state income taxes, or charitable giving could miss out on larger deductions.

- Not available to everyone. Your client cannot use the regular standard deduction if their spouse itemizes, if they're claimed as a dependent on someone else's return, or if they're a nonresident alien.

- One-size-fits-all. The standard deduction doesn't account for individual circumstances or unusually high deductible expenses in a given year.

What Are Itemized Deductions?

Itemized deductions work differently from the standard deduction. Instead of claiming a flat amount, your client tallies up qualifying expenses across several categories and deducts the total. More paperwork, but potentially more savings.

When a client itemizes, they list each deductible expense on Schedule A and attach it to their Form 1040. The IRS allows deductions in specific categories, each with its own rules and limits.

Categories of Itemized Deductions for 2025

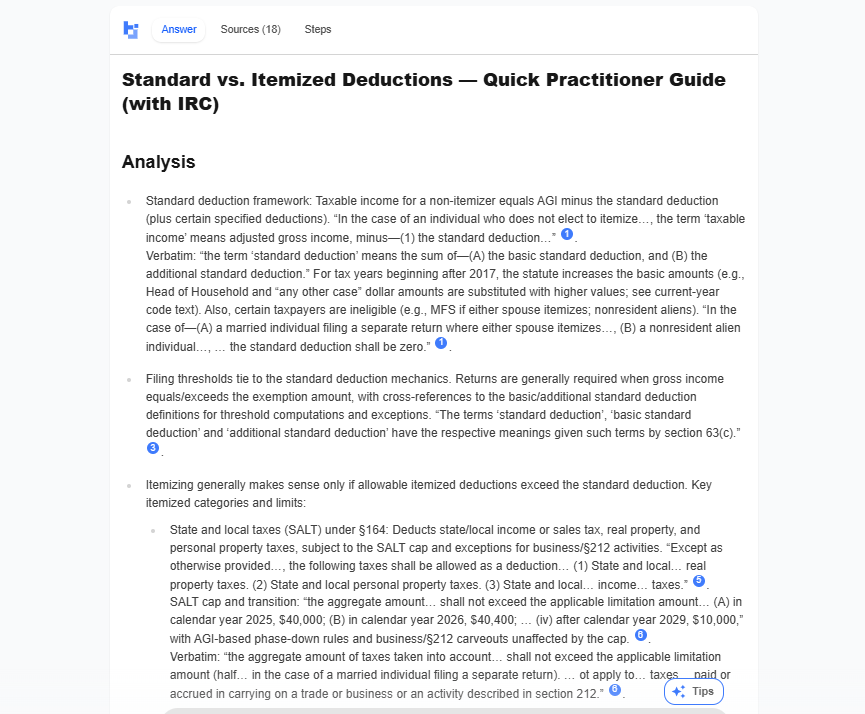

1. State and Local Taxes (SALT)

The SALT deduction covers state and local income taxes (or sales taxes if your client elects that option) plus property taxes. For years, the $10,000 cap made this deduction nearly irrelevant for high-tax-state clients.

The OBBBA raised the SALT cap to $40,000 for tax years 2025-2029, with married filing separately limited to $20,000. The cap also receives 1% annual indexing starting in 2026, reaching approximately $41,624 by 2029. This single change pushes many clients back into itemizing territory.

There's a phase-down for higher earners. Once MAGI exceeds $500,000 (single or joint) or $250,000 (married filing separately), the cap is reduced by 30% of income over the threshold. The cap floors at the original $10,000 limit, meaning high-income taxpayers still get the pre-OBBBA deduction but lose the enhanced benefit. Phase-down thresholds also receive 1% annual indexing.

For a married couple with $550,000 MAGI in 2025, the calculation works like this: $40,000 cap minus (30% × $50,000 excess) equals a $25,000 effective cap. At $600,000 MAGI, the cap reaches its $10,000 floor. This creates what practitioners call the "SALT torpedo," a zone between $500,000 and $600,000 where marginal tax rates spike artificially. Clients with MAGI approaching these thresholds need careful income timing analysis.

For clients below the phase-down, the expanded SALT cap is transformative. A California homeowner paying $25,000 in property taxes and $20,000 in state income tax was previously capped at $10,000. Now they can deduct the full $40,000.

2. Mortgage Interest

Homeowners can deduct interest on acquisition debt up to $750,000 ($375,000 for married filing separately). The OBBBA made this limit permanent after it was previously scheduled to revert to the pre-TCJA limit of $1 million after 2025.

Interest on home equity debt remains non-deductible unless the funds were used to buy, build, or substantially improve the residence securing the loan.

3. Charitable Contributions

Cash contributions to qualifying public charities remain deductible up to 60% of AGI. Appreciated property contributions are limited to 30% of AGI. The OBBBA made the 60% cash limit permanent.

Starting in 2026, a new 0.5% AGI floor applies to charitable deductions under Section 70425 of the OBBBA. Your clients will only deduct contributions exceeding this floor. For a client with $200,000 AGI making $10,000 in charitable contributions, only $9,000 is deductible because the first $1,000 (0.5% × $200,000) produces no tax benefit. Amounts below the floor do not carry forward. This makes 2025 the last year for full first-dollar charitable deductions.

4. Medical and Dental Expenses

Medical expenses exceeding 7.5% of AGI are deductible. The OBBBA made this threshold permanent, which is good news after years of uncertainty about potential increases to 10%.

For most clients, this deduction only kicks in during years with significant medical events. A client with $100,000 AGI needs more than $7,500 in unreimbursed medical expenses before any deduction applies.

Qualifying expenses include health insurance premiums (if not paid pre-tax), prescription medications, dental and vision care, long-term care premiums (subject to age-based limits), and transportation for medical purposes.

5. Casualty and Theft Losses

Personal casualty and theft losses remain limited to federally declared disaster areas. Your client cannot deduct losses from a house fire or car theft unless it occurred in a location where the President declared a major disaster. When deductible, losses are reduced by $100 per casualty and then by 10% of AGI.

A note on eliminated deductions: Several itemized deductions that existed before 2018 are gone permanently. The TCJA eliminated miscellaneous itemized deductions subject to the 2% AGI floor (investment advisory fees, tax preparation fees, unreimbursed employee expenses), moving expenses for anyone except active-duty military, and home equity interest unless used for home improvement. The OBBBA made these eliminations permanent, so if clients ask about these deductions, the answer is no.

Pros and Cons of Itemizing

Advantages:

- Potentially larger deduction. Clients with significant mortgage interest, high SALT, or substantial charitable giving often exceed the standard deduction by thousands of dollars.

- Reflects actual expenses. Itemizing captures your client's real financial situation rather than applying a one-size-fits-all amount.

- Greater tax savings for high earners. Taxpayers in higher brackets save more per dollar deducted. A client in the 32% bracket saves 32 cents for every additional dollar they itemize.

- The expanded SALT cap changes the math. The jump from $10,000 to $40,000 makes itemizing viable for millions of taxpayers who couldn't justify it before.

Disadvantages:

- Requires documentation. Your client needs receipts, 1098 forms, donation acknowledgment letters, and records for every expense claimed.

- More complex preparation. Itemizing takes significantly more time than claiming the standard deduction, both for your client in gathering documents and for you in preparing the return.

- Increased audit exposure. The IRS scrutinizes itemized deductions more closely than standard deductions, particularly charitable contributions and home office deductions.

- Variable from year to year. Your client's itemized total changes based on their expenses, which can fluctuate significantly. A year with low medical costs or reduced mortgage interest might push them back to the standard deduction.

How to Decide: Standard Deduction or Itemize?

The math is straightforward: your client should itemize when total itemized deductions exceed the standard deduction. The challenge is running that calculation efficiently for dozens of clients during busy season.

The Break-Even Calculation

For a married couple filing jointly in 2025, the threshold to beat is $31,500. Here's how to run the numbers:

- Add SALT. State income taxes (or sales taxes if higher) plus property taxes, capped at $40,000 or the phase-down amount for high earners.

- Add mortgage interest. Pull the 1098 figure. A $500,000 mortgage at 7% generates roughly $34,500 in first-year interest.

- Add charitable contributions. Cash and property donations to qualified organizations.

- Add medical expenses above threshold. Only amounts exceeding 7.5% of AGI count.

If the sum exceeds the applicable standard deduction, itemize. If not, take the standard deduction.

Quick Decision Guide by Client Type

Not every client needs a full calculation. For many, you can make a reasonable call based on their profile. Homeowners in high-tax states with mortgages almost always benefit from itemizing now that the SALT cap has expanded.

Renters in states without income tax rarely accumulate enough deductions to exceed the standard amount. Seniors who qualify for the bonus deduction face an unusually high bar because their standard deduction can reach $46,700 or more.

The table below summarizes common scenarios:

| Client Profile | Likely Best Choice | Why |

|---|---|---|

| Homeowner in CA, NY, NJ, CT with mortgage | Itemize | SALT + mortgage interest often exceeds $50K+ |

| Renter in low-tax state (TX, FL, WA) | Standard | No mortgage interest, minimal SALT |

| Senior 65+ with MAGI under $150K (MFJ) | Standard | Bonus deduction can push standard to $46,700 |

| High earner with MAGI over $500K | Itemize, but calculate SALT phase-down | May lose part of the enhanced SALT cap |

| Client with major medical year | Calculate both | Medical expenses could tip the balance |

| Large charitable giver | Itemize (and consider bunching in 2025) | 2026 introduces a 0.5% AGI floor |

Client Scenarios: Putting It All Together

Understanding when to itemize becomes clearer through real examples. These scenarios show how the analysis plays out for different client profiles. When you need to verify specific thresholds or confirm the rules mid-return, Bizora can pull the citation-backed answer in seconds so you're not digging through IRS publications.

Scenario 1: California Homeowner

Profile: Married couple, both 55, MAGI of $280,000, homeowners in San Francisco

Their numbers:

- State income tax: $22,000

- Property tax: $18,000

- Mortgage interest (on $650K loan at 6.5%): $41,500

- Charitable giving: $8,000

Here's Bizora's output for this scenario:

So, you can see that your itemized deductions (88.1k) far exceed the standard deduction (31.5k), so it's recommended you itemize.

The SALT cap doesn't bind beyond your 40k total in 2026, mortgage interest is fully within the 750k cap, and charity is reduced only by the 0.5% floor.

Scenario 2: Senior Couple in Texas

Profile: Married couple, both 68, MAGI of $85,000, renters in Texas (no state income tax)

Their numbers:

- State and local taxes: $4,500 (property tax on vehicles, sales tax)

- Mortgage interest: $0 (renters)

- Charitable giving: $6,000

- Medical expenses: $12,000 (above 7.5% AGI threshold: $5,625)

Here's Bizora's output for this scenario:

For this scenario, standard deduction is recommended as it exceeds their itemized total by over $30,000.

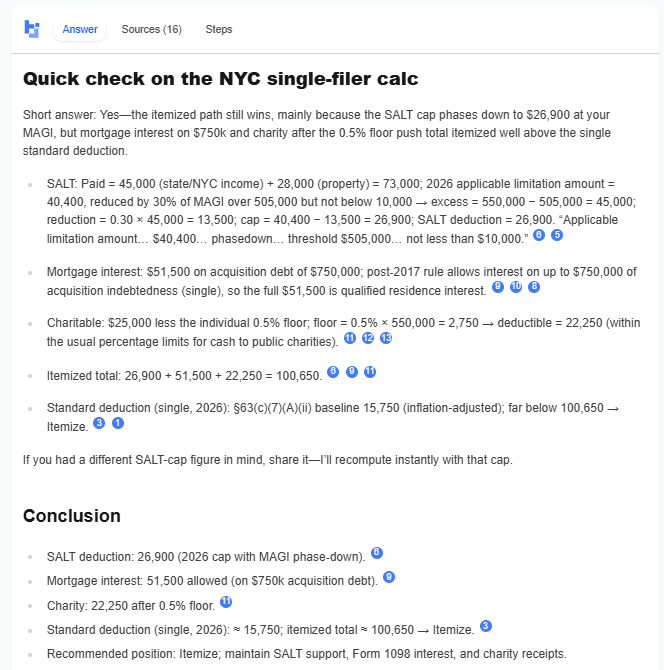

Scenario 3: High-Income Professional in SALT Phase-Down Zone

Profile: Single filer, 45, MAGI of $550,000, homeowner in New York City

Their numbers:

- State income tax: $45,000

- Property tax: $28,000

- Mortgage interest (on $750K loan at 7%): $51,500

- Charitable giving: $25,000

Here's Bizora's output for this scenario:

Now, for this scenario, the recommended deduction is the standard deduction.

With all these scenarios, you can see how having citation-backed research at your fingertips matters. Bizora AI backs each answer it gives you with citations.

So, when you're advising a client to time income around phase-down thresholds, you can confidently use it to help with researching underlying rules that may have otherwise taken hours to find.

Looking Ahead: What's Changing in 2026 and Beyond

While preparing 2025 returns, keep these upcoming changes on your radar for client conversations about future planning.

Charitable Deduction Floor (2026)

The new 0.5% AGI floor means clients will only deduct charitable contributions exceeding that threshold starting next year. Communicate this change now so clients can adjust their 2025 giving strategies accordingly. For clients who give consistently each year, bunching contributions into 2025 helps avoid losing the first-dollar deduction across multiple years of gifts.

Limitation on Itemized Deductions for Top Earners (2026)

Starting in 2026, the OBBBA adds a new wrinkle for top-bracket taxpayers. A reduction formula effectively caps the benefit of itemized deductions at roughly 35% instead of the full 37%, with SALT deductions hit harder than other categories. The exact calculation depends on how far income exceeds the top-bracket threshold. Worth digging into the statutory details before advising high-income clients on timing strategies.

SALT Cap Timeline

The enhanced $40,000 SALT cap runs through 2029 with 1% annual indexing, then reverts to $10,000 in 2030. Clients should understand this is a five-year window, not a permanent change. The income-based phase-down also disappears in 2030, meaning all taxpayers, regardless of income, will be limited to $10,000. Long-term planning may need adjustment as 2029 approaches.

Standard Deduction Inflation Adjustments

Expect continued inflation adjustments to standard deduction amounts each year. The IRS typically announces the following year's figures each fall. For 2026, standard deductions are already set: $16,100 (single), $32,200 (MFJ), $24,150 (HOH).

Conclusion

The standard vs. itemized deduction decision looks different in 2025 than it has in years. The quadrupled SALT cap, new senior deductions, and permanent thresholds create opportunities your clients didn't have before.

Don't assume last year's answer applies this year. Run the numbers for each client. The clients who benefited from the standard deduction for the past seven years may now come out ahead by itemizing. The reverse is true for seniors newly qualifying for the bonus deduction.

When you need to verify deduction limits or confirm the rules during busy season, Bizora delivers citation-backed answers in seconds. Your clients are counting on you to find every legitimate deduction, and the rules have changed enough that old assumptions need testing.

Frequently Asked Questions

What is the standard deduction for 2025?

For the 2025 tax year (returns filed in 2026), the standard deduction is $15,750 for single filers, $31,500 for married filing jointly, $23,625 for head of household, and $15,750 for married filing separately. Additional amounts apply for taxpayers who are 65 or older or who are blind.

Should I take the standard deduction or itemize?

Take whichever produces the larger deduction. Add up your itemized deductions including SALT (capped at $40,000 for 2025), mortgage interest, charitable contributions, and medical expenses above 7.5% of AGI. If the total exceeds your standard deduction amount, itemize. If not, take the standard deduction.

Can I take the standard deduction and itemize?

No. You must choose one method or the other for each tax year. You cannot claim both the standard deduction and itemized deductions on the same return. However, you can switch between methods from year to year based on which produces the better result.

What itemized deductions are no longer allowed?

Several deductions eliminated by the Tax Cuts and Jobs Act remain permanently unavailable: miscellaneous itemized deductions subject to the 2% AGI floor (including tax preparation fees, investment advisory fees, and unreimbursed employee expenses), moving expenses (except for active-duty military), and home equity loan interest unless the funds were used for home improvement.

What is the mortgage interest deduction limit for 2025?

Homeowners can deduct mortgage interest on acquisition debt up to $750,000 ($375,000 for married filing separately). The OBBBA made this limit permanent. Interest on home equity debt is only deductible if the funds were used to buy, build, or substantially improve the home securing the loan.

How do I calculate whether to itemize?

Add up your potential itemized deductions: SALT (up to $40,000), mortgage interest, charitable contributions, and medical expenses above 7.5% of AGI. Compare this total to the standard deduction for your filing status. Choose whichever amount is larger.